Stock-picking algorithms come in many flavors, most of which appear at first glance to be quite appetizing, but in the end are not very pleasing to the palate. But there is a small subset of these factor-based strategies that do produce gastronomical delight. What follows is a sector rotation stock screening algo that actually works. I know this because I’ve been using it with clients since 2010, and the proof is in the pudding.

OK, enough with the tortured metaphors already. Let’s get down to business.

The concept

In early 2010 one of my clients asked me what I knew about sector rotation strategies. Having no direct experience up to that time, I told him what I knew from reading about them. Sector rotation is a form of tactical asset allocation, where the investor makes portfolio rebalancing decisions based on what he or she believes to be the sectors of the stock market that have the greatest potential to outperform over the next year or so.

Until recently, there were 10 major sectors in the stock market. (Today there are 11 with the addition of Real Estate.) So the investor would begin the strategy by limiting his equity picks to just the top 2 or 3 sectors, and ignore the rest. At some predetermined point in the future, the investor would reevaluate the attractiveness of all the sectors and rebalance the portfolio accordingly.

It’s not a bad concept, but it’s time consuming to design, implement, and maintain a robust strategy. In order for it to work, it must be based on solid research, for both the sector choices and the stock (or stocks) that will represent the sector choices. Only a minority of investors, according to the academic literature at the time, were able to pull it off. Most of them abandoned the strategy after a year or two.

How I designed my sector rotation algorithm

In March of 2010 I began my research into sector rotation strategies by contacting the best research firm in that field at the time – Morgan Stanley. I had to open an account there in order to get access to their reports, but it was worth the trouble.

I proceeded to download every piece of information I could find on the subject. I studied their methodology, and asked for help from my rep at the firm. Long story short, I was able to piece together my own strategy based on what they were doing, but with some major adjustments.

Once I had a robust methodology for ranking sectors in order of their relative attractiveness, with a 12 month time horizon, I set about designing a methodology for ranking the stocks within each sector.

For this phase of the project I turned to the firm I considered the best in class at the time – Sanford C. Bernstein (now AllianceBernstein). I repeated the same process – open an account at the firm, download a bunch of reports, and enlist the help of my personal rep.

Now I had a working model of a sector rotation and stock picking strategy. I backtested it to 1990, and tweaked some parameters until I was satisfied that it worked the way I wanted.

Next, I called the client who had approached me with the idea and made the following proposition: If he was willing to take a chance on an unproven strategy, I would match his investment with my own money (using my own account, obviously). I couldn’t guarantee success, or promise to reimburse him for any losses, but at least he understood that I was willing to put my money where my mouth was. So he agreed.

Fast forward to today, and this client is still invested in the strategy. And in fact he has added to it regularly over the years. Over the 6 years since implementation, the results have been very good. The average annual alpha (performance in excess of the market return) is 3.87%, with no losing years. If you don’t think that’s a big deal, just plug the numbers into your favorite retirement calculator (widely available for free online) and see what happens to your money.

I now have 128 participants in the strategy, who receive a monthly report from me (with updates more frequently if needed), and the list continues to grow. I make no claim that my strategy is the best one out there, but I can say that it works as expected. There are other strategies that claim to produce more alpha than mine, but their results are more volatile. My strategy is designed to minimize risk, so my clients are happy to make a little less in exchange for more consistent results.

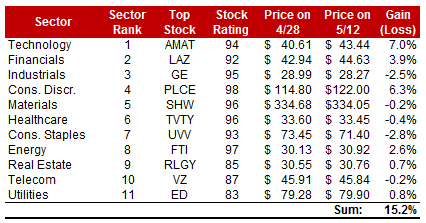

Below is a table that shows the most recent picks, which were made on May 1, 2017. I run the algorithm once per month and publish the new list. Some names stay on the list, some drop off. Most clients limit their portfolios to the top 2 or 3 market sectors, so that means 6 trades per month, max (3 sells, 3 buys).

It’s best to do this in a tax-deferred account if possible, but the alpha is large enough to make a net profit even after paying short-term capital gains. If you want to learn more about how this strategy works, email me at info@zeninvestor.org