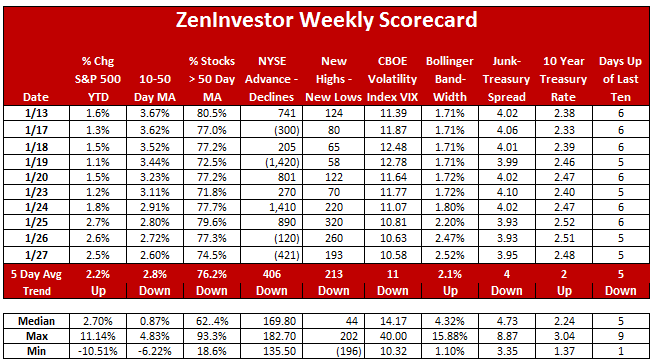

Weekly Market Scorecard – January 27, 2017

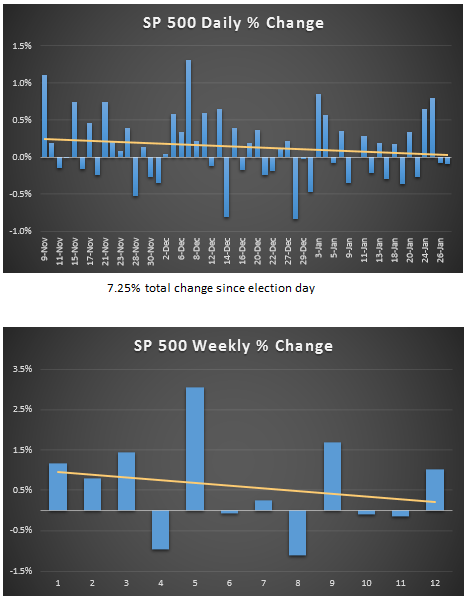

- The S&P 500 is up 20.8% from a year ago.

- It’s up 7.2% just since the election.

- The rally is being driven by investor optimism.

- Optimism is based on certain key expectations.

- One major key is earnings expectations.

- We look at earnings trends for each of the major sectors.

Before we get to earnings, let’s review the market internals for the two weeks just passed.

The stock market is off to a good start. Investors are optimistic about the future, and they have high expectations that Trump will deliver on his major campaign promises. Specifically, large tax cuts for corporations, significant deregulation for businesses, massive spending on infrastructure and the border wall, and the renegotiation of trade deals like NAFTA.

But maybe the most important promise of all was Trump’s pledge to bring back high-paying manufacturing jobs that have moved offshore and decimated our manufacturing sector. I think this one will be the hardest to achieve.

There are several risks to the current market rally. One is that the Republican House and Senate could decide to slow the process of implementing Trump’s agenda. Even if they don’t oppose it outright or try to kill it, slowing it down may be enough to take some of the optimism out of the market. The market is vulnerable because investors have bid up prices to reflect the (mostly) full implementation of the Trump agenda.

Short-term momentum, as measured by the gap between the 10 day moving average and the 50 day, is a still-healthy 2.60% but the gap has been narrowing over the last three weeks. This tells me that traders with shorter time frames are starting to pull back just a little.

Market breadth, as measured by the percentage of stocks that are above their 50 day moving average, the advance-decline line, and the number of stocks making new highs minus those making new lows, is now narrowing after widening for the last couple of months. It’s too early to tell whether this is a change of trend, but it bears watching.

Volatility, as measured by the VIX and Bollinger Band readings, is low. Investors are optimistic and confident that better days lie ahead. But I think they may be overconfident about how quickly those better days will arrive. I expect the VIX and the Bollinger Bands to move higher as the reality of a slow-moving Congress becomes apparent.

The spread between junk bond rates and Treasury bond rates is narrowing, which supports the idea that investors are confident about taking more risk in their search for yield.

Lastly, the number of up days out of the last ten trading days is at a neutral reading of 5.

Now let’s take a closer look at the vaunted Trump Rally, and take note of not just the upward price trajectory, but the rate of change in the trajectory. As I’ve pointed out before, the rate of change has been weakening since the first week after the election in November. The market is clearly moving higher, and even setting new records along the way, but we shouldn’t ignore the pace of increase. It may give us clues about how committed investors are to the rally.

The Trump Rally

As you can see, the market is up, but the pace of the increase is slowing. The yellow line on the above charts is a simple trend line, which shows a pronounced downward trajectory of both daily and weekly gains in the market.

Earnings expectations are driving the market

After an earnings recession that lasted for 5 quarters, year-over-year earnings growth finally turned positive last quarter, and are shaping up to be even more positive this quarter. (See chart below.)

Investors and analysts now expect earnings to continue rising for the foreseeable future. It’s this optimism that is helping to drive the market higher and make a new string of records, including Dow 20,000.

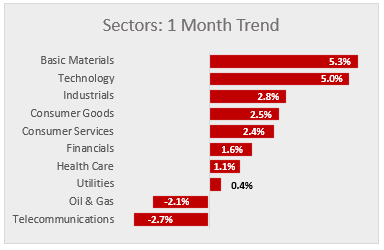

Drilling down to look at Sector earnings growth

The pickup in earnings has been driven to a large degree by the energy sector. The oil price has rebounded nicely over the last year, and many of the projects that were suspended are opening and making money again.

Finance is another standout, boosted by two factors. The increase in short term and long term interest rates are helping profit margins for lenders, and the anticipation of significant deregulation for the banks is creating an expectation for more business activity overall.

Expectations for large spending on infrastructure is driving up prices for Basic Materials, Construction, and Industrial Products. The chart below shows how each major sector is doing so far this quarter, and how analysts think they will do when all the earnings data has been released.

Top performing market sectors

Looking at the one month performance of the ten primary market sectors we can see that Basic Materials, Technology, and Industrials have been leading the market higher. Telecom and Utilities are yield plays, and they tend to lose favor when growth is dominant. Oil & Gas has given back some of the large gains of the past year, but that’s to be expected.

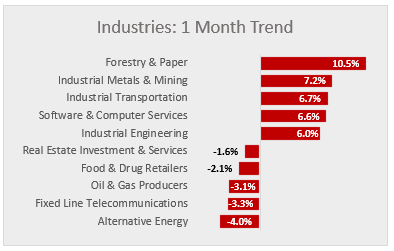

Top performing industries

The surprise of the last month is the strong performance of the Forestry & Paper industry. I admit that I’m a little baffled about what may be driving this move, but I think there’s something going on. It might just be a reversion to the mean, or it could be industry consolidation.

Alternative Energy reversed again, after putting in a nice showing the last few weeks. It’s no secret that Trump and his cabinet are friendly to the fossil fuel industry, so I expect alternatives to get less support going forward.

Some takeaways

The bulls are clearly in charge. But I think that certain risks in the market are increasing. Valuations are stretched, investors are showing signs of complacency, and expectations for a fast rebound in earnings might be too aggressive.

From a geopolitical perspective, Trump appears to be embarking on a strategy that keeps both our enemies and our allies a little on edge. That may be an effective negotiating tactic in the boardroom, but the market doesn’t like uncertainty.

Trump has a golden opportunity to boost economic growth, bring back factory jobs, and renegotiate unfair trade deals. I hope he will deliver on these promises.

“In the short term, the market is a voting machine.

In the long term, it’s a weighing machine.”

-Ben Graham