The next bear market could be a Doozy. (A technical term.)

Do you remember the Global Financial Crisis (GFC) of 2007-2008? If you do, you know it was a doozy. Economies and stock markets around the world crashed, and there was serious talk about a possible meltdown of the entire financial system.

Do you think something like that can happen again, or do you think that policy makers have taken steps to prevent it? Your answer to that question says a lot about how naïve you are.

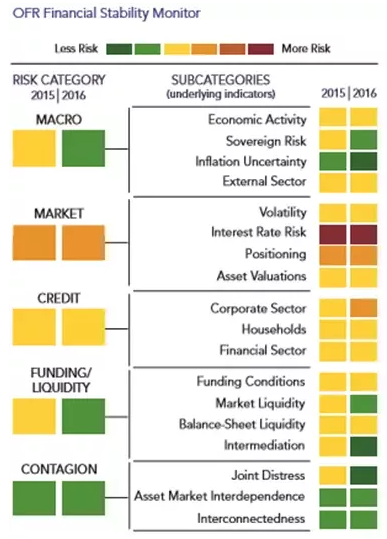

The Office of Financial Research (OFR), a branch of the U. S. Treasury, publishes an annual report on the state of the global financial system. Here’s a chart from the most recent report.

There is a lot going on in this chart. Most of the indicators are green or yellow, which indicates that the financial system is currently stable. Some risks have increased, and others decreased since the last GFC.

Interest rate risks and market risks are a concern. Credit risks in the corporate sector also look troubling.

The financial system is extremely complex and adaptive to changes in the economy. That makes it nearly impossible to predict when, or if, things will go haywire. The system is driven by the psychology of billions of people, with diverse agendas, and random events across the globe.

The stock market is driven by algorithms and models that can breakdown or oversimplify complexity. Chaos theory tells us that a complex, adaptive system will behave in unpredictable ways. As long as we have an interconnected global financial system, we will have financial crises. There’s no avoiding it.

Threats to the Global Financial System

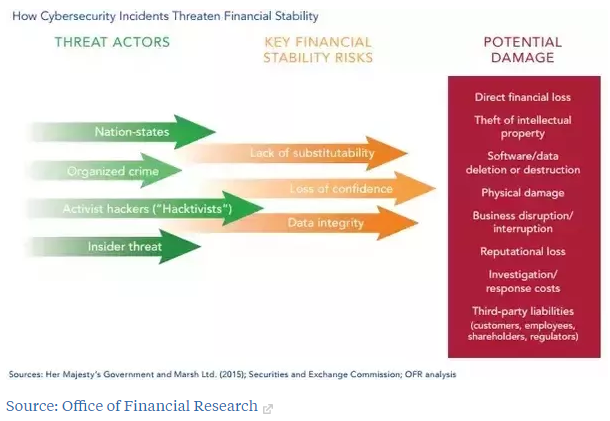

A Cybersecurity Incident

Cyber-attacks are something everyone has heard about. I believe that most of us underestimate the seriousness of these attacks. Most of our financial system exists in digital form in the cloud. This makes it vulnerable to cyberattacks.

A successful cyberattack can cost a financial institution money, reputation, sensitive customer information, and possibly its ability to function at all. This can cause major panic and disruption in the financial system. Look at the graph below for a visualization of this threat:

Politics and Populism

Politics and the rise of populism are another concern. Politicians pandering to certain groups can end up making serious policy mistakes. A notable example is the brinkmanship with the US debt ceiling and the threat of a U.S. Treasury default a few years ago. This default would have led to a self-inflicted financial crisis, but thankfully it was averted.

Another example is the sabre rattling between the U.S. and North Korea. This kind of bluster and intimidation belongs in a bar at midnight, not in the geopolitical arena where both sides have the potential to kill millions of innocent civilians.

I believe that a shooting war between these two nuclear powers would cause so much panic, that the stock market would tank and the global financial system would be tested.

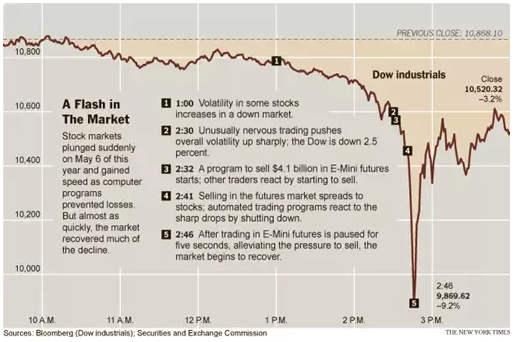

Algorithmic Trading and Regulation

Technology and regulation are constantly changing the structure of financial markets. High frequency trading can create stronger feedback loops and regulation can have unintended consequences. These factors may lead to unpredictable flash crashes and market disruptions. Look at the graph below for a visualization of the 2010 flash crash.

Financial innovation

Financial technology (Fintech) companies are bringing innovative new financial products to the market, but they come with financial risks that may not be well understood, and in some cases not understood at all. When regulators don’t understand the risks, they can’t design effective rules to prevent harm to the system. These risks could cause the next crisis.

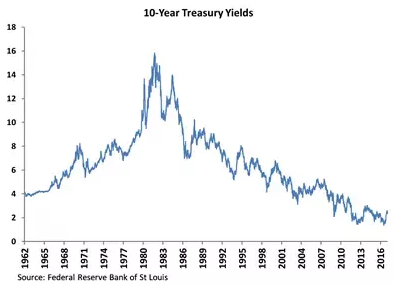

Chronically Low Interest Rates

Who doesn’t love low interest rates? Home buyers love them. Corporations love them. Stock market investors love them. But low rates are a double-edged sword. Retirees living on a fixed income hate them. Insurance companies who have promised higher payouts hate them. Pension funds trying to fund their future obligations hate them.

Interest rates have been declining since 1980, and they have remained low for an extended period (see graph). These low interest rates create incentives for financial market participants to take increasing amounts of risks to get better returns. This can create high levels of systemic risk in the financial system and leave many financial institutions and investors more vulnerable to rises in interest rates, loss of liquidity, or other market and credit shocks. Prudent regulation and risk management is especially critical in a low interest rate environment.

High Levels of Corporate Debt

Low interest rates have helped fuel the growth in non-financial corporate debt (see graph). This is because many investors want higher interests than they can get from safe Treasury securities, so they invest more in riskier corporate debt.

However, when the business cycle eventually turns, there will be higher rates of default for these securities. If investors are properly diversified and practice sound risk management, these losses should be manageable. If they are not, the banks, mutual funds, life insurers, and pension funds that hold most of this non-financial corporate credit will take losses and their systemic importance can lead to greater financial instability.

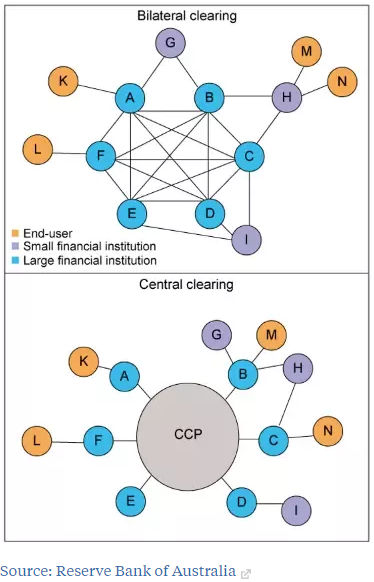

Counterparty Risks

Central counterparties (CCPs) have become a key part of the post-financial crisis reforms. CCPs sound complicated but they are designed to simplify the process of handling the delivery and payment of financial transactions.

Risks in the financial system are often hedged by derivatives (derivatives can also be used for pure speculation.) A concern with derivatives is that one of the parties to the contract might go bankrupt before the contract expires. This is called counterparty risk.

A remedy for this has been to create CCPs to specialize in guaranteeing counterparty performance, ideally improving risk management and market transparency. However, there are concerns that the push towards central clearing has concentrated too much risk in one place (see graph), making the failure of a major CCP a serious financial stability concern.

Life insurance companies

Life insurance companies are an increasing source of risk. Given the low interest rate environment, they are incentivized to take greater risk to meet their obligations to policy holders. The failure of a large and interconnected insurer (like AIG during the last GFC) or a shock to all life insurers has been identified as a major financial stability concern by OFR.

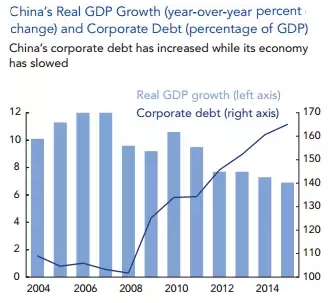

China

China is dealing with a high corporate debt load and transitioning towards a consumption and service oriented economy with slower growth (see graph). The transition has been smooth so far, but it can easily go off track and pose a major financial risk. Given the size and importance of the Chinese economy, its problems will almost certainly affect the rest of the world.

Eurozone Breakup

The Eurozone was formed in 1999 and created a common currency for its members. This helped increase the flow of capital into countries like Greece, Portugal, Italy, Spain, and Ireland that previously had a harder time attracting financing. However, instead of making productive investments, many of these countries have used the debt to fuel consumption and speculation.

When the last GFC hit, investors reassessed their investments and pulled their money from these countries, causing major stress to their economies and financial system. Ever since, there has been a fear that there would be a disorderly breakup of the Eurozone causing even more financial instability that will in turn affect the rest of the world.

The Shadow Banking System

Shadow banks are financial intermediaries that like banks borrow short-term and lend long-term. However, unlike banks they can’t borrow from the Federal Reserve nor have access to Federal Deposit Insurance. This makes them highly susceptible to runs during periods of stress. Shadow banks include money market mutual funds, repurchase agreements, investment banks, and mortgage companies. The run on shadow banks helped fuel the 2008 financial crisis. Another run on the shadow banking system is still a risk.

Commercial Real Estate

There has been a rise in lending to and prices for commercial real estate (see graph.) This sector is vulnerable to a turn in the business cycle and a crash can affect small and mid-size banks that generally make commercial real estate loans. Troubles at these banks could result in some financial stability problems.

The Stock Market

US stock prices seem high when adjusting for the business cycle and earnings. This suggests we are in a stock market bubble that might crash soon. The largest stock market crash in U.S. history was in 1987 and had no real effect on the economy, but it would be foolish not to at least be somewhat concerned about a crash today.

The Known, Known-Unknown, and Unknown-Unknown Risks

“Someone asked me recently what risks keep me up at night. I worry most about the risks I understand the least. Where are our blind spots? Has the continuous evolution and innovation in the financial system caused a build-up or risks in a part of the system where we are not looking? The unknown risks are what keep me up at night.”

-Richard Berner, Director of the Office of Financial Research