What do Warren Buffett, George Soros, Carl Icahn, Ray Dalio, Abigail Johnson, James Simons, Thomas Peterffy, Ron Perelman, and Steve Cohen all have in common? They are all highly accomplished investors. And they make up 9 out of the 10 richest Americans, according to Forbes, Inc.

Introduction

The fact that 9 out of the 10 richest Americans made their fortunes in the investment business is no accident. They are all very smart, highly skilled, and extremely accomplished investors who operate in one of the most lucrative industries on earth.

Before I get into the characteristics, or traits, that these investors have in common, let me define a few terms. I use the term “accomplished” to describe the highest level of skill and achievement for an investor. One level down from accomplished is “high-performing.” This class of investors share many of the same skills and characteristics that their betters have, but they have not yet mastered the ability to capitalize fully on their formidable talents. Put another way, they leave too much money on the table.

The next level of achievement is “competence.” This can almost sound like a left-handed compliment, but it’s high praise indeed. In order to achieve competence in investing, one must overcome a gauntlet of challenges, including capital market theory, crowd psychology, behavioral economics, and brutally honest self-awareness. In my experience, less than 5% of the investing population will ever master these skills and achieve true competence.

List of Characteristics

1. Experience

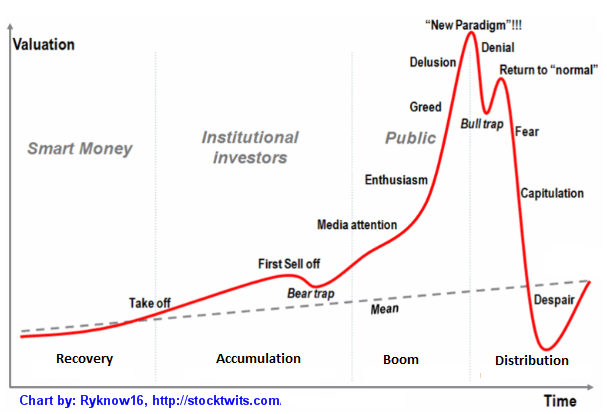

Experience is an essential attribute in becoming a competent investor. It is impossible to become proficient in investing without having experienced at least one full market cycle that includes both a bull and a bear phase. Full market cycles take about 4 years to complete, on average.

We can divide a market cycle into four phases: recovery, accumulation, boom, and distribution.

Recovery. After a bear market has finally come to an end, and it starts to level out, the recovery phase begins. The so-called Smart Money (investment banks, hedge funds, sophisticated investors) quietly begin to pick up high-quality stocks at bargain-basement prices. These are the early adopters.

Accumulation. As the market continues to rise from the depths of the previous bear, institutional investors begin to accumulate more stocks. The financial media notices this and begins to change the tone of their market coverage from pessimistic to optimistic.

Boom. Once it starts to become clear that the bear market has ended and a new bull market has begun, the public (retail investors) joins the party and starts buying in earnest. The market accelerates rapidly, and finally the last holdouts throw in the towel and join in. These unfortunate souls are driven by FOMO (fear of missing out). Since everyone else is already invested, the latecomers have nowhere to go when the market tops out. There are no buyers left in the market.

Distribution. The smart money and the institutions are first to sense that a market top is approaching, so they are the ones who are selling to the latecomers. They switch from accumulation (net buying) to distribution (net selling). After they are out of the market, the public starts to recognize what’s happening and they add more selling pressure to the declining market. What starts out as a routine dip in prices turns into a correction, and finally into a full-blown bear market.

Each of these phases of the market cycle requires an awareness of the unique dynamics at work. Only by living through these changing market conditions can an investor come to fully understand the game.

2. Intelligence

It may surprise you to learn that raw intelligence (as measured by I.Q.) is not a reliable predictor of investing competence. In fact, some studies I’ve seen indicate that investors with a very high I.Q are more susceptible to overconfidence than investors with an average I.Q. Overconfidence is a killer in investing. It not only leads to very expensive mistakes, it also hinders the ability to learn from these mistakes. That’s a double-whammy.

In my experience, someone with a 120 I.Q. who thinks he’s a 110 is more likely to succeed than a 140 I.Q. who thinks he’s a 160. The former has humility and the latter has hubris. Humility is a winner every time. As Warren Buffett famously said, “The most important quality for an investor is temperament, not intellect.”

3. Self-Awareness

Self-awareness is a trait that is difficult, but not impossible, to learn – if you weren’t fortunate enough to have been born with it. It requires a willingness to look inward, and make an honest accounting of your tendencies towards biased thinking and flawed logic. It’s very hard to do, even for someone like a trained psychologist. But again, it’s not impossible.

The rewards for putting forth the effort to become a more self-aware investor are substantial. You will not repeat the same mistakes as often. You will tend to avoid giving in to emotional impulses that have gotten you into trouble in the past. And you will be in a better position to find a strategy that fits well with your natural instincts and decision-making style.

4. Situational Awareness

While self-awareness is all about turning inward, situational awareness is about turning outward. It’s about seeing reality as it is, rather than as you wish it to be. Are you the type of person who is quick to conclude that sometimes things just don’t add up? The many ways in which this skill translates into the avoidance of a disaster are obvious. A stock that appears to be unbelievably cheap might be cheap for good reasons. A strategy that seems too good to be true might be bogus. Whenever I find myself salivating to buy a great stock that has been dropping sharply in price, the first thing I want to know is… who is selling it? Do they know something that I don’t?

5. Math Skills

Investing is filled with lots of third or fourth-grade level mathematics when it comes to odds, ratios and other percentage plays that can boost your chances for success. Understanding basic probability theory will go a long way. Here’s the good news: All of the math that you will need to achieve competence as an investor can be learned in 10 hours or less.

6. Willingness to Learn

No matter how much experience and intelligence you have, you will not reach true competence as an investor unless you are open to learning from your own mistakes, and the wisdom of those who came before you. This can be done through books, training videos, one-on-one coaching or exchanging ideas with someone you look up to. If you think you have it all figured out, you’re probably doomed.

7. Ability to Control Emotions

In investing, it is always important to have a logical, rational basis for what you are doing. Our emotions are not equipped to deal with probability and randomness, which are two defining elements of investing.

The ability to control your emotions in order to make rational decisions consistently is one of the hardest things for investors to master.

8. Discipline

The most successful investors know when to stick to their guns and when to cut their losses. You won’t win on every trade, and you should work hard to admit to yourself when you’re on the wrong side. Having discipline as an investor is not as hard as you might think. If you take the time to develop a plan, formulate a strategy, set specific money-management rules, and have a Plan B ready for contingencies, the rest is automatic.

9. Patience

Investors become competent when they give their strategy enough time to work. I have seen countless investors abandon a strategy at the first sign of trouble. They impatiently move on to the next shiny object that catches their attention. Instead of viewing a short-term loss as a defeat, why not take it as an opportunity to learn and improve your skill set?

10. Adaptability

The best investors are good at adapting to changing circumstances. When the facts on the ground change, they ask themselves whether their assumptions are still valid. What they don’t do is bail out of a trade, or a strategy, simply because it has become uncomfortable.

11. Risk management

Finding a great strategy is all well and good, but it’s all for naught if you can’t stay in the game. Keep a record of your most and least successful trades, and adjust your bets accordingly. If your staying power will be compromised by a potential loss on a strategy or a trade, it’s time to rethink it.

What’s Next?

In the next installment of this series on characteristics of highly accomplished investors, I will drill down into the details with the goal of giving you a realistic picture of what it takes to achieve competence as an investor. Once you achieve competence, it becomes a matter of desire and commitment to move beyond that.