What’s your number? Your number is the amount of money it would take to enable you to retire and live off the interest without touching the principal.

Your number is the very definition of financial security, and “hitting your number” is the Holy Grail of every retirement plan. We’re going to look at some of the ways you can get to your number by saving and investing, and you can use this information to make some important decisions about how much to save and invest.

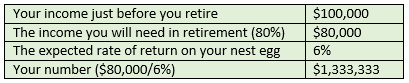

Let’s say you’re just starting out in a career that will ultimately span 40 years. You’re 25 years old, and your income is $25,000. Over time – with raises, promotions, and job changes – you end up earning four times as much as your starting income, or $100,000 per year. The first question is how much income will you need when you retire, in order to have a comfortable standard of living? Financial planners estimate that you will need about 80% of your pre-retirement income when you retire, which works out to $80,000 in this case.

Simple Arithmetic

The next question is, how much will you need to have in your account when you retire, so that you can live off the interest? The answer is $1.3 million. Here’s how we got to this number.

How realistic is it for you to accumulate a $1.3 million nest egg over a 40 year career? The answer depends on two things: how much are you willing to save, and what rate of return will you get on your investments. Let’s look at each of these factors.

Save More

How much of your income would you need to save in order to accumulate a nest egg of $1.3 million? The answer is 50%. That’s right – you would have to save half of your gross income every year in order to reach your number by saving. But this isn’t realistic. It will be difficult enough just to manage to put away 10% of your income. So let’s look at another way to get to the number – by getting a better return on your investments.

Invest Smarter

Let’s go back to saving 10% of your gross income, but now let’s increase your return on investments. Up until now we’ve been assuming that the return on investments is 4%, which just matches inflation. The net effect is that investments have not contributed to our nest egg. But let’s see what happens when you increase the investment return to 7% and to 11%. How will that impact the size of your nest egg?

What does this table reveal? That the rate of return on your investments is critically important to your financial security in retirement. If you earn 4% then all of your investment gains will be wiped out by inflation, and you will be living off principal and your nest egg will be depleted in less than 4 years. If you earn 7% then your nest egg will be a little bigger at the beginning of retirement, but you will still deplete it in 6.2 years. It’s only when you earn 11% on your investments that you begin to build a nest egg that’s large enough to sustain you for long enough in retirement so that you can be financially secure.

How To Get 11% Return

How do you get 11% return on your investments? It’s not as hard as you might think. You would have to match the average rate of return of the stock market, and reduce your market exposure during economic recessions. There are some excellent economic forecasting services available that do a great job of calling recessions. NoSpinForecast is one. RecessionAlert is another. And my own premium newsletter includes a recession forecast.

But the problem is that the average investor only makes 4%, not 11% on investments. Why is this? It’s mostly due to poor timing. The typical stock market cycle is long periods of rising prices, interrupted by short periods of declines, usually caused by economic recessions. The average investor waits until the economy is so bad that the stock market is down 20% or more, at which point they get worried enough to sell their stocks. When the economy recovers, they are hesitant to get back in because they are worried about losing more money. So they wait until the evidence is clear that the recession is over, and they get back into the stock market at much higher prices. This poor timing is the main reason why the average investor only makes 4% per year on their investments, while the stock market goes up by 11% per year, on average.

Alternate Views

Steve Vernon is research scholar for the financial security division of the Stanford Center on Longevity. His book “Money for Life” discusses the pros and cons of various ways to generate retirement income. Here’s what he has to say about “the number.”

“My very general rule of thumb is to have savings equal to 25 times your desired amount of annual retirement income when you retire. So if you need $100,000 per year in retirement income, you’ll need $2.5 million in savings. If the $100,000 income is in addition to Social Security or includes Social Security, that makes a difference.” (I excluded Social Security in my calculations, so the $2.5 million figure is what I’ll use for Mr. Vernon’s version.)

BlackRock, the asset management company, has a retirement calculator that shows the amount an investor must save in order to generate a desired income throughout retirement. Using the same parameters given to Mr. Vernon, the BlackRock calculator comes up with a slightly lower result: $2 million. That would require savings of about $9,500 per year from age 20, based on a projected annual return of 6%. That’s an achievable number if you have a 401(k) plan; in fact, it’s well below the $17,500 maximum deferral that the IRS allowed in 2014.

But it is about $800 every month. That’s a big number to someone in their 20s. And it only gets worse (harder to save enough) as you get older. That’s why I believe that the best way to get to your number is by combining both strategies – saving more, and earning a higher return on what you’re saving. The good news for most investors is that Social Security income will provide some support to the effort of hitting your number. A person who works for 40 years, and ends with a final salary of $100,000, can expect Social Security to kick in at least 20% of the income needed in retirement. So the numbers are going to be a little less intimidating than they seem in the above examples.

ZenInvestor Premium subscribers learn how to set up their portfolios to capture the full 11% return. For more information on how to do this, send a message to us at info@zeninvestor.org