Investment advice is a great business. It has a business model with fat profit margins and a sticky, recurring revenue stream. And the beauty part is that most of the clients have no idea how much they are actually paying, or what they’re getting in return.

I challenge you to find an example of another business where a high school dropout with an average I.Q. and mediocre math skills but a knack for telling a great story can end up making $500k per year without breaking the law (or breaking a sweat).

That’s easy, you say. Be an entrepreneur – start a business – it’s the American Dream! This country was built on the sweat and toil of risk takers with little education but a fire in their belly and a novel idea. Granted. Those people are out there. But here’s the difference between an entrepreneur and an investment adviser.

An entrepreneur puts up all the capital and takes all the risk that’s required to turn her vision into a successful business. But an investment adviser puts up zero percent of the capital (it’s the client’s money), takes zero percent of the risk (the client takes all the risk), and yet ends up pocketing as much as 80% of the profits on the deal. Nice work if you can get it!

This is not an original idea. Jack Bogle, founder of the Vanguard Group, is the one who came up with the idea that financial intermediaries pocket 80% of the profits that rightfully belong to the client. But in order to get to 80% he stretched his assumptions to their limit, by using an investment time frame of 65 years. While this is certainly possible for some investors, I ran the numbers using what I think is a more realistic time frame of 40 years. I also made a few other changes to Mr. Bogle’s assumptions with the intention of making the numbers more realistic.

I assumed that a typical investor began saving and investing for retirement at the age of 25, and continued to work and contribute to savings for the next 40 years until retiring at 65. Bogle was right in arguing that retirement doesn’t mean the end of paying fees on the portfolio, which is why his analysis continued for another 25 years. But I wanted to be more conservative in my analysis, so I used 40 years instead.

The typical investor in my example begins with an annual salary of $25,000. I assumed annual income growth of 3%. That may seem unrealistically high, but you have to account for the likely events where she changes employers to improve her prospects and her income. Most workers won’t jump to a new job unless there is an opportunity for a raise of 10% or more. So I think my assumption about a 3% annual income growth is realistic.

I also assumed that she saves 10% of income, on average. Again, this may seem unrealistic. But with company matching and higher contributions later in life, I think it’s a reasonable assumption.

I assumed a nominal return for the portfolio of 8%. Again, I think it’s justified. The long term return on stocks is about 9.5%. Here’s what our intrepid (but average) investor can expect to accumulate over a 40 year investing time frame.

Using the assumptions I described above, she will accumulate a total of $962,222 by the time she retires at 65 years of age. Of this amount, $188,603 came from her monthly contributions to the account. In other words, her own money. The rest – $773,619 – came from the 8% returns she got from the market each year, on average. At this point, she should be in a position to retire in relative comfort and maintain the lifestyle she had in her last year of working.

But now comes the harsh reality of paying for investment advice. To keep the math as simple as possible, I broke the cost of investing down into 3 broad categories: mutual fund or ETF expense ratios, trading costs, and adviser fees. Here’s what each of these costs works out to, on average, over the last 10 years.

It’s fair to say that most investors today are paying something close to the 2.5% shown in the table above. There are some who are paying less, for example those who have big accounts (more than $1Million) and have negotiated a lower rate with their adviser. (Even wealthy and experienced investors are probably paying other fees that are not easily identified.)

If you’re asking yourself “what’s the big deal? 2.5% doesn’t seem like much of a fee to pay for something as valuable as professional advice about how to invest my life savings.” But it is a big deal, for two reasons.

- What you’re paying for is the growth of your nest egg, but that’s not what you’re being charged for. That 2.5% is based on your entire account value, not just the growth of your account. Don’t think of it as 2.5% of 100%. Think of it as 2.5% of 8%, which is the assumed rate of growth you’re paying for. Your adviser is offering you a deal where he or she will deliver a product – 8% growth – and you have to pay 2.5% of that 8%. The harsh reality is that you’re really paying 31.25%, not 2.5%.

- The deal you made isn’t really a deal at all, because the adviser doesn’t have to deliver on the 8% return he showed you in his sales pitch.

If your account only grows 5% this year, he won’t make it up to you. But you still have to pay the same 2.5%. Only now you’re really paying 50% of your earnings to him. And what do you think will happen when the market goes down, and your return is minus 8%? It’s a double-whammy. Not only do you lose out on the 8% gain you expected, based on the colorful charts and graphs he showed you, but you are still on the hook for the 2.5% fee that was part of the deal you made.

But wait a second, you say. How can I pay 2.5% of nothing, or in this case less than nothing? The answer is that your fee is based on your total account balance, and it’s not affected by what happens in the market. The business model used in the advice industry requires you to accept these terms. Even the regulators are on board with it. Advisers are prohibited by law from reimbursing you for any losses you incur, unless it was due to their own malfeasance. In that case, you would have to sue them in order to collect. Your case would probably go to mandatory arbitration and be decided by a panel of “industry experts.”

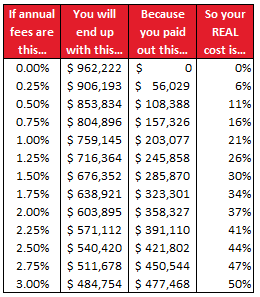

The table below shows the impact on your nest egg after 40 years of earning 8% in the market. The far left column is the total cost as a percent of your account balance. The next column shows the final value of your nest egg at retirement 40 years from now. The third column is the total amount of your nest egg that you paid out, directly and indirectly. The last column shows your REAL cost.

Let’s pretend for a minute that you are the best negotiator in the world, and you found a way to invest at zero cost. In that case, you will have accumulated a $962,222 nest egg after 40 years. But if we assume, as I did for the purpose of this article, that you are more like the typical investor, paying all-in fees of 2.5%, then you will have handed over $421,802 of your nest egg to “the system”. That’s 44% of your account value.

So the takeaway is that expenses matter – a lot. There are things you can do about this. You can fire your expensive adviser and handle everything for yourself. You can invest in ultra-low cost index funds. You’ve heard it all before, but the fact is that investors are still paying out 30, 40, and 50% of their potential lifetime wealth even today.

What about a Robo-advisor like Schwab Intelligent Portfolio, that claims to offer advice for free? My advice is to read the fine print. There is no such thing as a not-for-profit investment firm with all volunteer employees.