Have you drunk the buy-and-hold Kool-Aid?

If so, don’t worry – it might be the best approach for you. After all, when Warren Buffett endorses a strategy, how bad could it be? This article shines a light on a significant flaw in the entire premise of buy-and-hold as a universally superior strategy.

What’s the big deal about bear markets?

Bear markets are rare events. They come along every 6.2 years, on average, and they typically take a 34% bite out of your savings. That certainly stings, but the whole painful episode is over relatively quickly. Traditional bears last about a year-and-a-half, on average. For most investors, the easiest way to deal with a traditional bear is to simply ride it out. You take a 34% hit to your wallet, but you get it all back in a year-and-a-half. Or do you?

The answer depends on the way you think about your money. If you think about your money as a number in your bank account, or the balance on your brokerage account statement, then you’re a traditional investor. You don’t look beyond the change in the balance of your account. As a traditional investor, you see bear markets in a traditional way. For you, waiting out a bear market is painful, but not devastating.

But what if you’re not a traditional investor? What if you’re capable of next-level thinking, and see money in a more practical way? Money is indeed a number in your bank account, but that’s not all it is. What money really is, is buying power. Buying power is the real value of money after adjusting for inflation. It’s not the number in your account that maters, it’s how much you can buy with it.

Super-bear markets are traditional bear markets, but with one important difference: they take inflation into account. That makes them more realistic, because buying power is what counts. These Super-bears are even more harmful than traditional bears, because they don’t end until your buying power is made whole again.

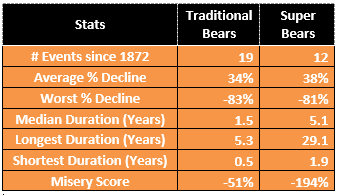

Anatomy of a Super-bear

Super-bears happen every 12.1 years, on average, compared to 6.2 years for traditional bears. But Super-bears are far more destructive than they appear. They inflict more pain, and last much longer than traditional bears. The following table compares these two types of bear markets.

The real cost of a Super-bear is not the percent decline from peak to trough. No, the real cost is the amount of time lost. Think about that for a minute. Money is a renewable asset. If you lose money, you can go out and get some more. But time is not renewable. It’s fixed. And when you go through a Super-bear, you are losing more than 5 years of the precious time you have been allotted as a living member of the human race. That’s pretty serious, IMO.

In my view, Super-bears should be avoided if possible. Buy-and-hold works, but only if you see money as a number in your bank account. Who cares about a year-and-a-half in the grand scheme of things, right? But if it’s going to cost me 5 years to get whole again, I’m not willing to sit quietly and just take the pain. I’m going to play some defense.

This brings us to the next question: what is the likelihood that a new Super-bear is coming, sometime within the next 12 months? Thanks to the work of Thomas Bayes, an 18th century English statistician, philosopher and Presbyterian minister, we have the ability to answer this question.

Defining the solution methodology

Bayes came up with a way to calculate the probability of an event in a very creative way. He started with a simple accounting of the “base rate” probability by counting the number of times the event has happened in the past.

Then he went a step further. He adjusted the base rate probability by taking into account new information that came to light. For example, the probability of getting into a car crash is 1 in 6,700 (according to Harvard School of Public Health). That’s the base rate. But if you are drunk, the probability goes up by 5 times, making the odds 1 in 1,340.

What Bayes did was take the base rate of 1 in 6,700 and adjust it to take into account that the driver is drunk. You might think that the odds go up to 1 in 1,340 but they don’t. The base rate still applies in the calculation. The additional information (drunk driver) raises the odds of an accident, but not all the way. The true odds are somewhere between the base rate and the drunk driver rate.

Applying the solution methodology to the stock market

Now let’s turn our attention to the question at hand: What is the likelihood that a Super-bear market is coming, sometime in the next 12 months? Here’s how Bayes would answer our question.

Let A represent the event that a Super-bear market is present (SBM). We define a SBM as a condition where the current market price is at least 20% lower than its most recent all-time high price.

Let B represent the event that a dip in the market is present (DIP). We define a dip as a condition where the current market price is at least 5% lower than its most recent all-time high price.

In this scenario, it is possible for B to be present and A to not be present simultaneously, but not the other way around. If A is present, then B must also be present, by definition.

What is the probability of A? (the prior probability of a bear market being present).

What is the probability of B? (the condition where the market is down by 5% or more).

What is the probability of B given A? (the probability of a 5% decline, after a 20% decline has happened).

What is the probability of A given B? (the probability of a 20% decline, after a 5% decline has happened).

Based on historical data, the probability of A, the market being down by 20% or more, is .325.

Based on historical data, the probability of B, the market being down by 5% or more, is .673.

Bayes would say that the prior, or base rate, probability that a new bear market is coming sometime in the next 12 months is 32.5%. He arrived at this number by adding up all of the days where the market was at least 20% below its most recent all-time-high, and dividing that number by the total number of days in his dataset.

Next, he wanted to know how the probability changed if the market was already down by at least 5%. The idea is simple – market prices exhibit momentum, and once a trend is in place, the market often (but not always) continues to move in the direction of the trend. Or as a physicist might say, an object in motion tends to stay in motion.

We already know that the probability of the market being down at least 5% from its all-time high is .673. Bayes’ genius was figuring out a way to use this new information to adjust the base rate (.325) and arrive at a new probability.

This new probability is what he called the posterior probability. The posterior probability of a Super-bear coming within the next year, when the market is already down by 5%, is 0.61 or 61%. Put another way, when the market is already down by 5%, the probability of a Super-bear nearly doubles from 32.5% to 61%.

There are many other factors that influence the likelihood of a bear market, and each of them can be measured and used to fine-tune the base rate probability of .325. I chose the DIP condition (down 5%) to illustrate how the Bayesian methodology works.

What is the lesson to be learned from this?

If a market price dip of 5% can double the likelihood of a bear market happening, then what other conditions can come into play? And how much do they influence the odds? One of the most reliable factors is the onset of an economic recession. Almost every recession in the last 100 years has been accompanied by a bear market. But there have also been several instances where a bear market happens without the help of a recession. The Bayes method provides a way to measure the influence of the various factors that correlate with bear markets, like recessions do.

As I said earlier, it’s one thing to ride out a bear market that takes 1.5 years to recover from. In fact, this is the rationality used by the investment industry to convince investors that buy-and-hold is always the best way to go. They tell you that trying to “time the market” is a fool’s errand.

But I wholeheartedly disagree. When we look at bear markets in terms of purchasing power, rather than a simple number in our brokerage account, we can see the devastation that these events cause. Why would anyone willingly give up 5 years of returns with a buy-and-hold strategy? Wouldn’t it make more sense to take some defensive action, in order to shorten the amount of time lost to a Super-bear? I think the answer is an unequivocal yes.

Using Bayesian probability, we can arrive at a reasonably accurate answer to the question of “what are the odds of a bear market coming within the next year?” Let’s say that you are 10 years from retirement. You have probably cut your equity exposure to about 50%. Then along comes Mr. Bayes, who says to you, “the odds of a bear market coming in the next 12 months is 80%.” Are you really going to gamble your retirement fund on the possibility that he could be wrong? And if he is right, are you willing to gamble that your retirement account will fully recover by the time you stop working?

I wouldn’t take those risks. Even if I were in my 30’s I wouldn’t take those risks. Every investor must decide for him/herself what the tipping point is for them to begin playing defense. That part is a personal choice based on your risk preferences. But as the odds go up, the argument for buy-and-hold gets weaker.

There are low-cost ways to play defense. For example, a simple moving average system will get you out of the market before most of the damage is done. A recession-based system is also very effective. And simply cutting back on your equity exposure as valuations become stretched, as they are today, is another way.

I’m not a fan of all-in or all-out market timing, but tactical asset allocation when done systematically can add several percentage points to your annual returns, and save you from years of being “under water.”

Excellent article!